Tough new legislation is on the horizon to regulate the operations of licensed money lenders in Hong Kong, aiming to build a more transparent money-lending sector, combat unscrupulous malpractice and prevent borrowers from being caught in a vicious debt spiral or over-indebtedness. Li Xiaoyun reports.

Even with Hong Kong’s bank base rate now standing at 4 percent, interest rates in the credit market can still soar up to 48 percent legally — 12 times the official benchmark. This is the reality of what industry insiders call the “fourth tier” of credit: the licensed money-lending sector.

Licensed money lenders, known locally as finance companies, operate outside the special administrative region’s three-tier banking system, offering quick loan approvals and light documentation but, typically, charging much higher interest rates than banks.

The irony of such a lending market extends beyond its high legal rates. Without a comprehensive information-sharing system, lenders are often left in the dark about borrowers’ overall liabilities. The data gap allows borrowers to take out loans from multiple lenders simultaneously, trapping them in a vicious cycle of “robbing Peter to pay Paul”.

In one extreme case, Andy (identified under a pseudonym to protect his identity) had secured loans from more than 30 licensed lenders to service existing obligations, but saw his debts balloon to over HK$6 million ($770,000) in just nine months.

The fallout from debt spirals often ensnares more than just the borrower. Some people have had their personal information given to money lenders without their knowledge, leaving them named as “loan referees”. Unlike guarantors, these referees have no legal liability for repayment, but are often subjected to persistent debt collection calls when borrowers default. This loophole has made innocent third parties targets of collectors.

The sector’s persistent volatility stems from a regulatory framework that has struggled to keep pace with the modern financial landscape. Hong Kong’s Money Lenders Ordinance, in force since 1980, originally set a criminal interest rate ceiling at 60 percent per annum and established a 48-percent threshold above which loans could be deemed as “extortionate”. These limits have remained unchanged for more than four decades even as bank prime lending rates have fallen from double-digit levels in the 1980s to about 5 percent in recent years.

In 2022, the statutory cap was lowered to 48 percent and the threshold for the “extortionate” rate was reduced to 36 percent in one of the most significant amendments to the ordinance since its introduction.

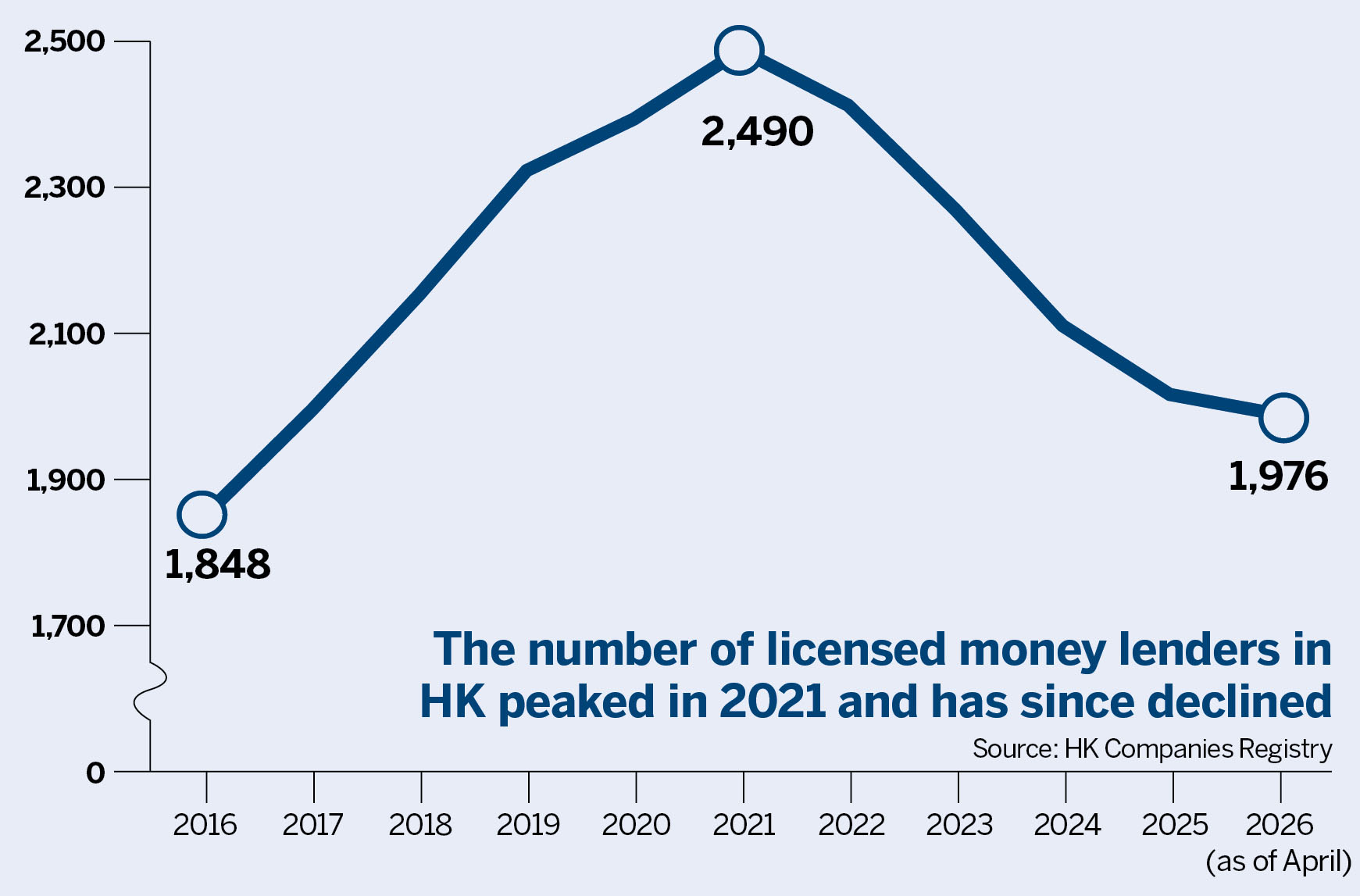

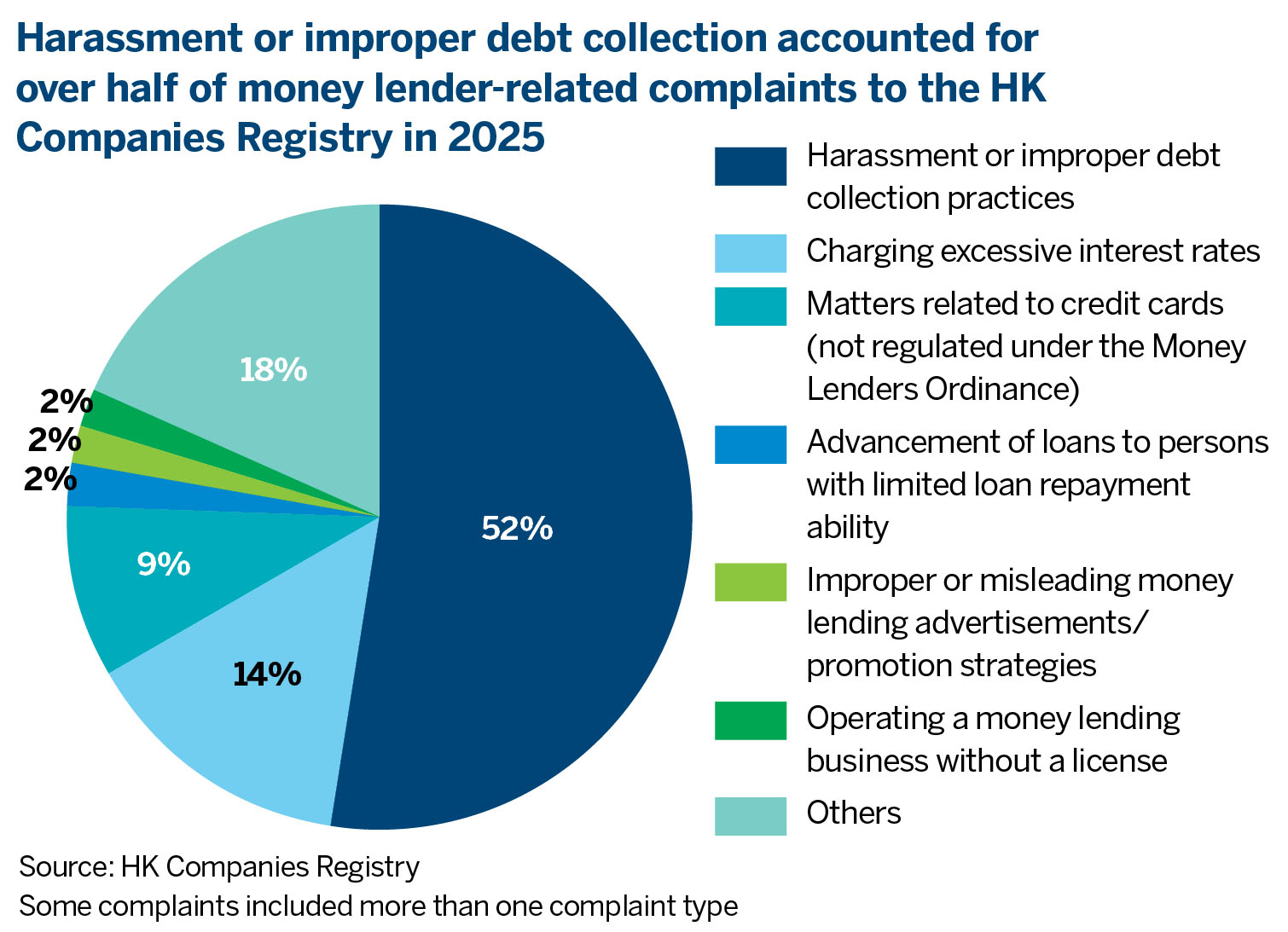

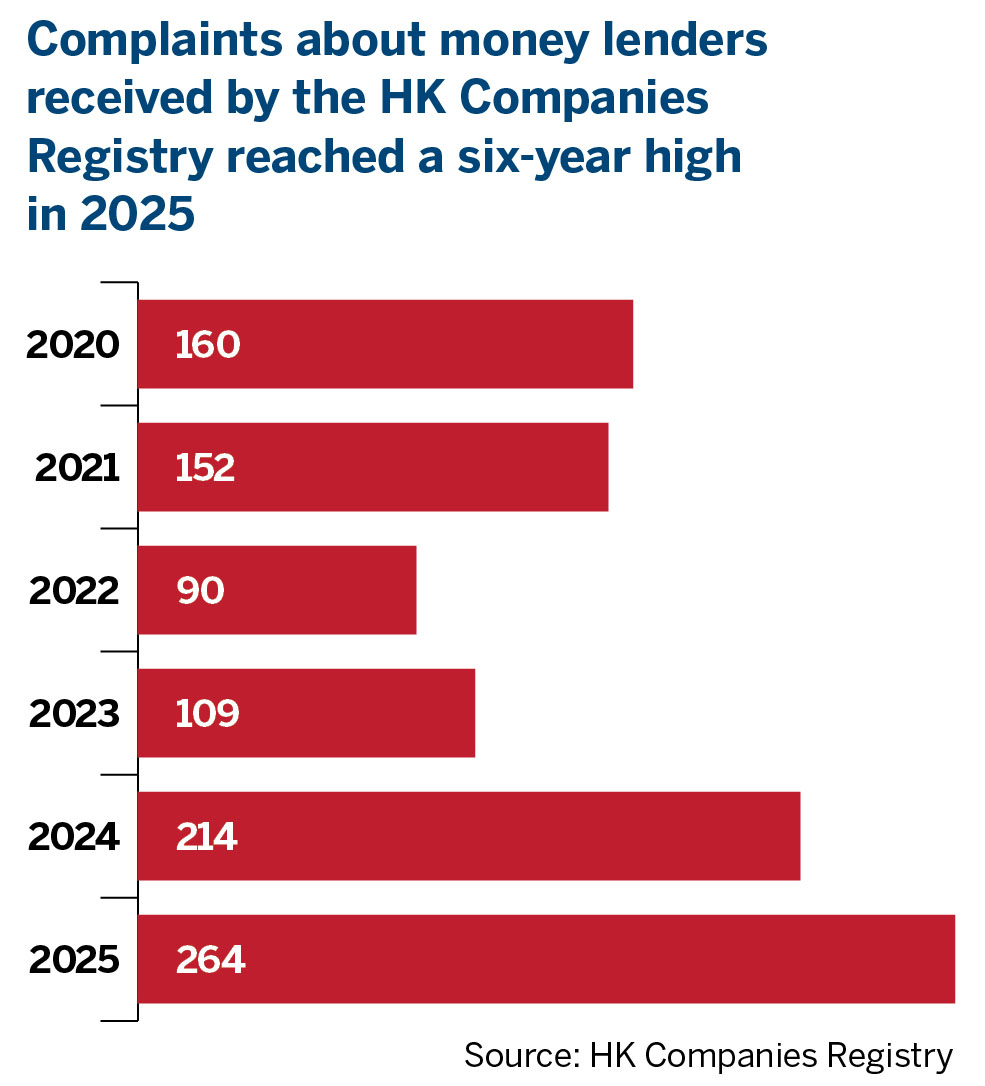

However, this sharp reduction in interest rates was still far from sufficient to quell misconduct. The Companies Registry received 264 complaints last year alone — a six-year high and nearly triple the number recorded in 2022. More than half of them were concerned with harassment or improper debt-collection practices, with excessive interest charges being the second most common grievance.

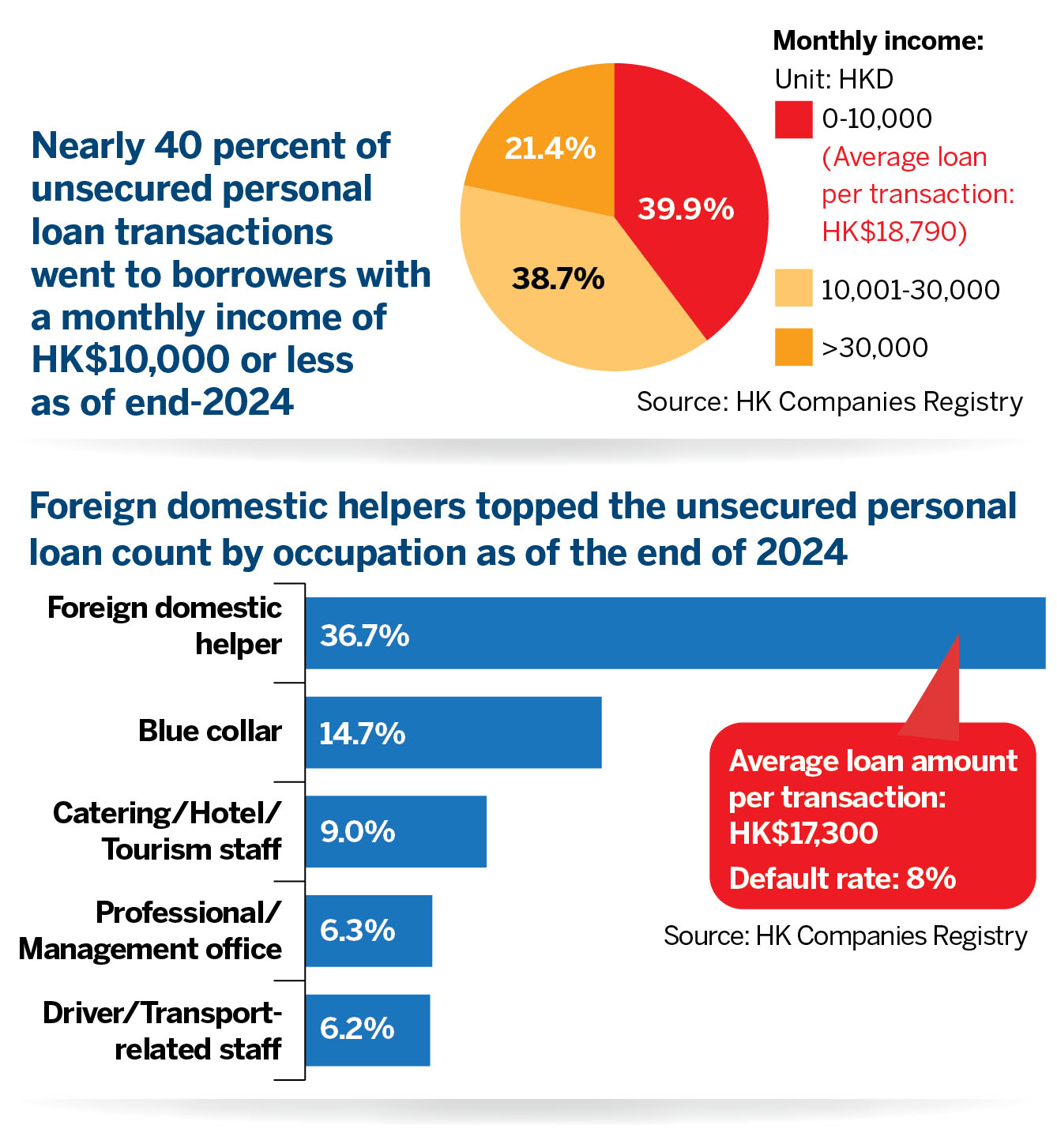

According to the Financial Services and the Treasury Bureau (FSTB), over-borrowing is acute among lower-income groups. Foreign domestic helpers account for the largest share of unsecured personal loans from licensed lenders and the helpers have the highest default rates. When they are unable to repay or leave Hong Kong without settling debts, their employers, often listed as referees, are frequently harassed by debt collectors.

Keeping pace with change

Against this backdrop, the FSTB said it is determined to strengthen the regulation of licensed money lenders and unveiled a two-phase reform package in March this year following public consultations.

The first phase, due to take effect in August, will cap the share of income that low-earning borrowers can devote to loan repayments, with the aim of ensuring they can meet basic living costs and avoid being caught in a debt spiral. The much-criticized practice of requiring borrowers to provide loan referees will also be scrapped.

The second phase, regarded as a cornerstone of the overhaul, centers on Credit Data Smart — a credit-information sharing platform. It will require all money lenders offering unsecured personal loans to submit borrower data and, in some cases, consult the database when assessing loan applications. Aimed at eliminating the trap of “robbing Peter to pay Paul”, the initiative is due to be implemented in June next year. Cases like Andy’s, in which loans were secured from several lenders in quick succession, could therefore be mitigated.

Bill Tang Ka-piu, a Hong Kong lawmaker who represented the Hong Kong Federation of Trade Unions during the FSTB’s policy consultation process, says the new measures are intended to address the public’s most pressing concerns through administrative means.

As for issues that remain unsolved but contentious, he says the government has pledged to conduct further studies next year when statutory amendments may be on the table.

The new regulatory framework is expected to phase out some non-compliant and small-scale money lenders, leading to a consolidation of market resources toward larger operators with stronger transparency and compliance standards, says a spokesperson for the Licensed Money Lenders Association.

However, tighter access to regulated credit could also raise concerns that some borrowers may turn to unregulated, illegal lenders as an alternative, the spokesperson warns. “A dual-track approach is essential. The Hong Kong SAR government should simultaneously intensify enforcement action against illegal lending syndicates while strengthening the regulatory framework.”

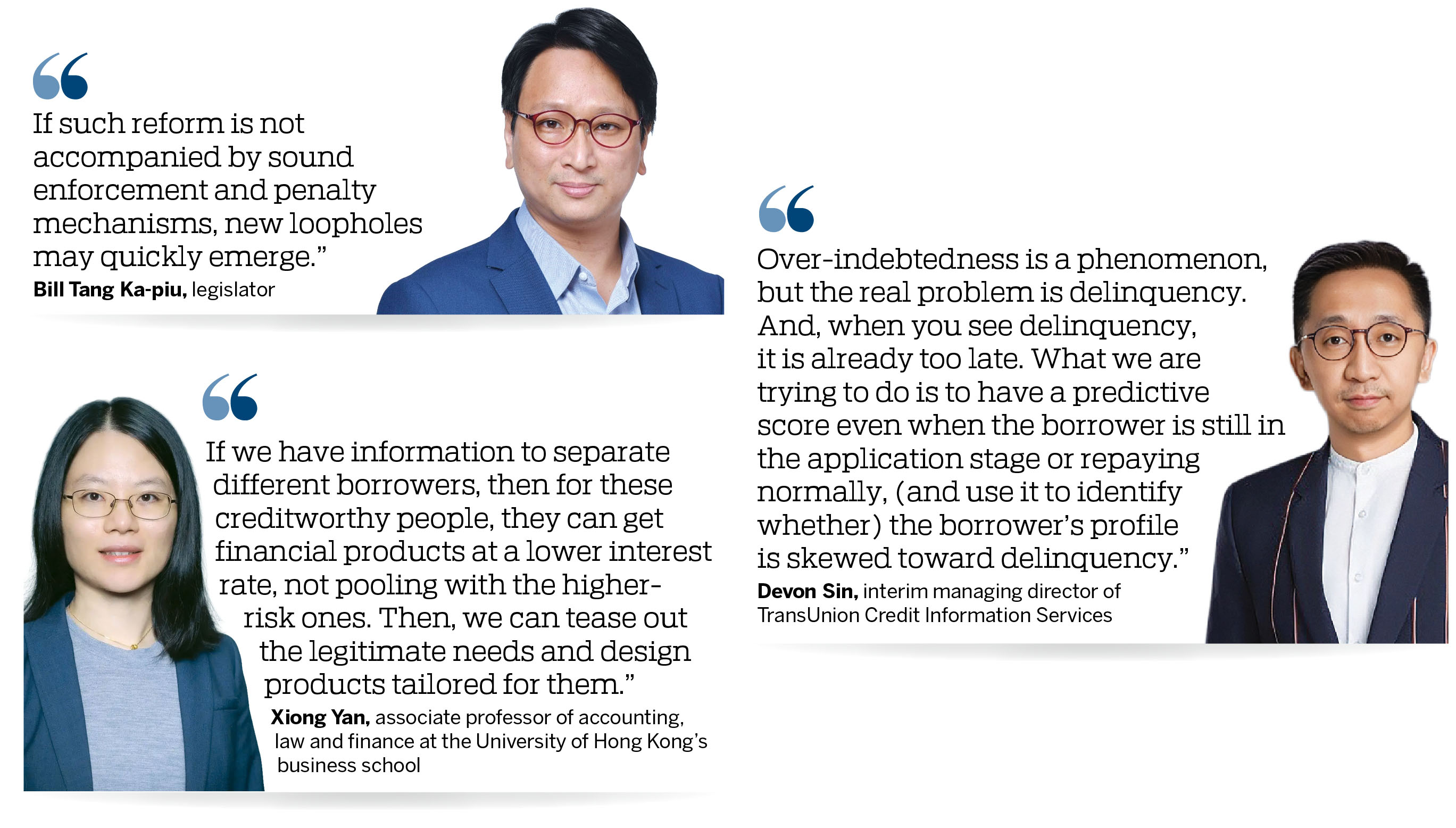

Tang agrees that regulatory architecture alone is inadequate, cautioning that “if such reform is not accompanied by sound enforcement and penalty mechanisms, new loopholes might quickly emerge”.

Taking the soon-to-be-banned “loan referees” as an example, he says lenders intent on skirting the rules could simply rebrand referees as “introducers”, or go further by dangling inducements to coax borrowers into surrendering the personal details of friends and relatives to facilitate future debt collection.

Filling the banking gaps

For all the controversy surrounding the money lending sector, few would dispute its role in Hong Kong’s financial system.

Unsecured personal loans — the lightning rod for public criticism — account for about one-third of licensed money lending business, according to Xiong Yan, an associate professor of accounting, law and finance at the University of Hong Kong’s business school. Secured lending, mainly backed by residential property, makes up a larger share, at roughly 40 to 50 percent.

With banks constrained by a 70-percent loan-to-value cap on residential mortgages, borrowers seeking additional liquidity cannot secure a second mortgage against the same property within the banking system. In such cases, Xiong says, many turn to licensed money lenders for top-up loans, and some also tap these lenders to fill gaps in their down payments.

The rest of the sector’s portfolio includes loans to small and medium-sized enterprises that fall short of banks’ credit thresholds, but require rapid working capital, as well as a small proportion of auto loans.

Xiong describes licensed money lenders as “a necessary part” of Hong Kong’s financial system and a “complement” to its three-tier banking structure of licensed banks, restricted license banks and deposit-taking companies. Barred from absorbing public deposits and operating outside the Hong Kong Monetary Authority’s regulations, licensed money lenders are a de facto “fourth tier” of credit provision.

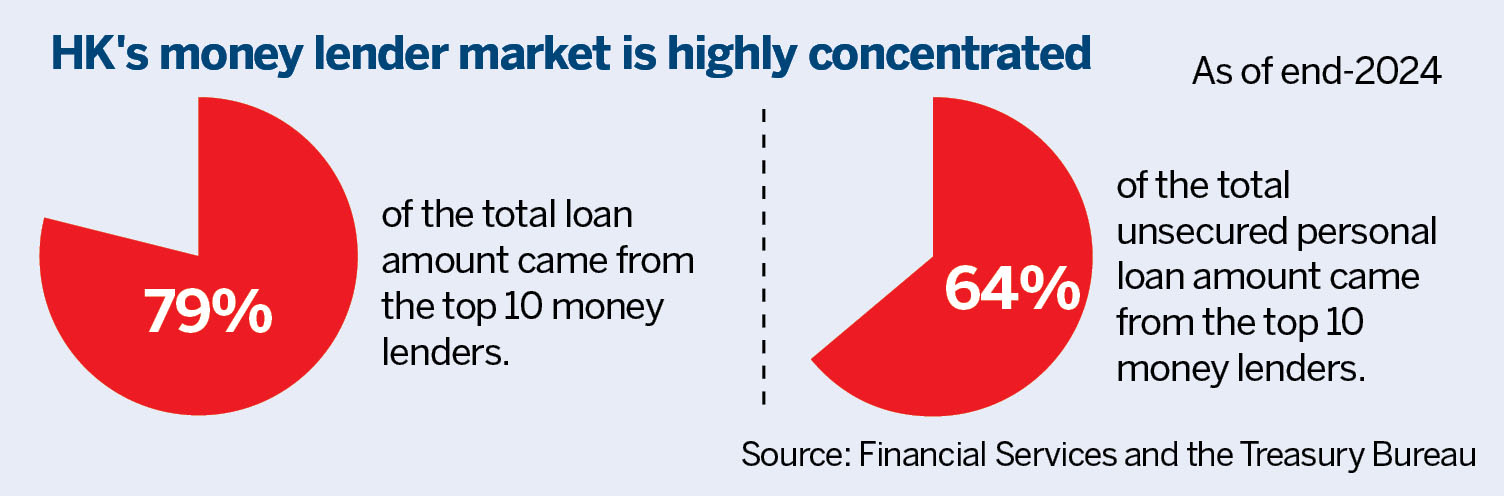

The fourth-tier credit market serves as a vital financial lifeline for those excluded from mainstream banking. According to the Companies Registry, lower-income borrowers form a substantial constituency of the unsecured market. At licensed lenders with at least HK$10 million in outstanding unsecured personal loans, borrowers earning HK$10,000 or less per month accounted for 29 percent of transactions in 2023, although the city’s median monthly wage is more than double that level.

Compared with banks, money lenders operate with a wider risk appetite and a client base skewed away from super-prime borrowers, says Devon Sin, interim managing director of TransUnion Credit Information Services — a credit reference agency that supplies loan applicants’ reports to banks and licensed money lenders.

These non-bank lenders can afford to be “more aggressive and creative” in the products they offer, while banks that fund themselves with public deposits lend more conservatively, he adds.

Sin says measures related to Credit Data Smart, set to begin in June 2027, are expected to enhance data completeness, thereby reducing the risk that licensed money lenders make flawed or incomplete credit decisions due to insufficient understanding about borrowers’ credit profiles.

The government estimates that about 340 lenders, accounting for about 94 percent of the unsecured personal-loan market, will ultimately be required to use Credit Data Smart in assessing applications.

Beyond traditional scoring

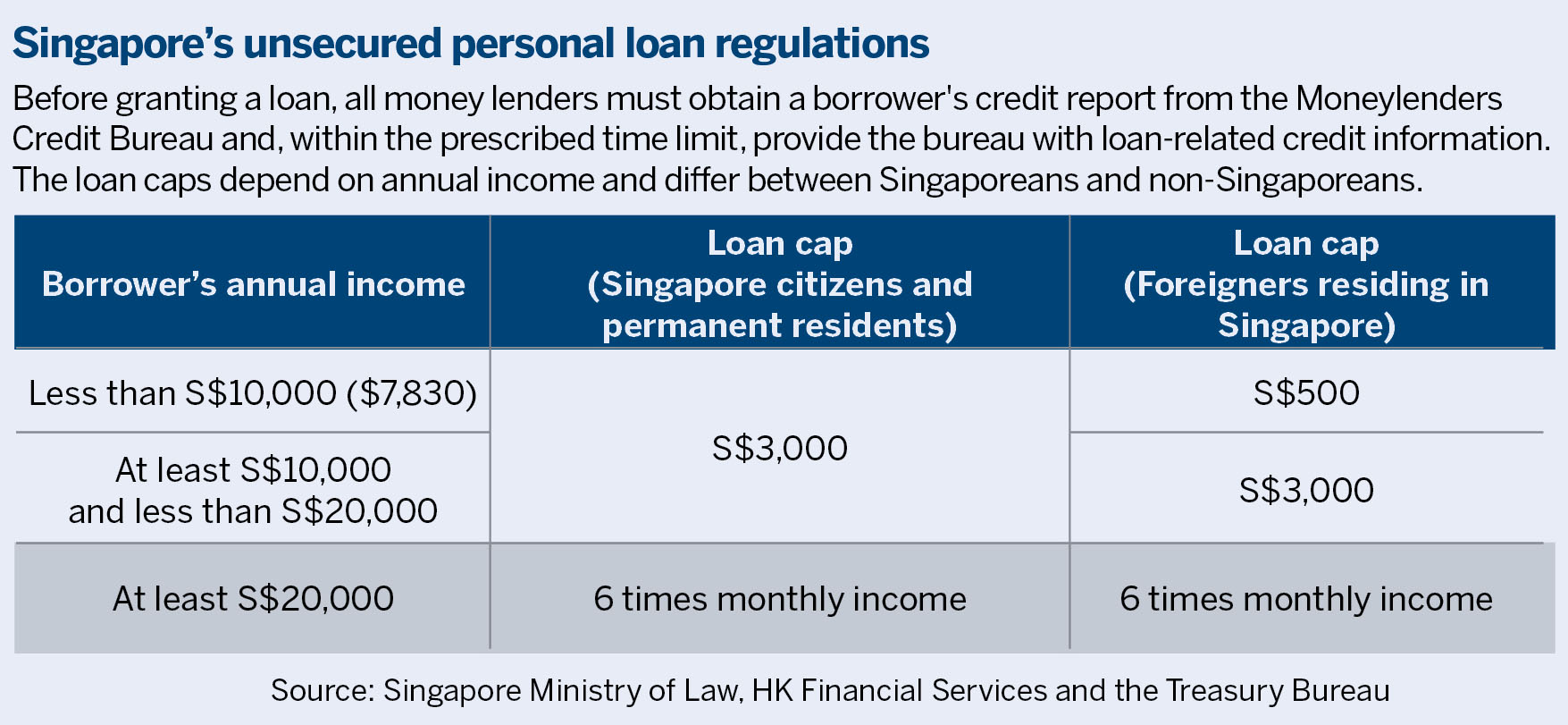

The approach is similar to reforms introduced in Singapore a decade ago, although the city-state’s regime is more comprehensive.

Since March 2016, all licensed money lenders in Singapore, not merely the largest players as in Hong Kong’s case, are required to purchase a borrower’s credit report from the Moneylenders Credit Bureau before extending a loan. They must also submit details like a loan’s tenure, the interest rate and repayment schedule to the central data repository.

Still, Credit Data Smart is a constructive first step in giving the industry access to more information and is key to Hong Kong’s regulatory overhaul, Xiong says, although this alone may not suffice.

Preventing over-indebtedness, she argues, ultimately depends more on having comprehensive information to differentiate borrowers by risk and to price credit accordingly.

Given the variation in borrowers’ credit quality, a uniform interest-rate cap at 48 percent is a blunt approach. “If we have information to separate different borrowers, then for these creditworthy people, they can get financial products at a lower interest rate, not pooling with the higher-risk ones,” Xiong says. “We can then tease out the legitimate needs and design products tailored for them.”

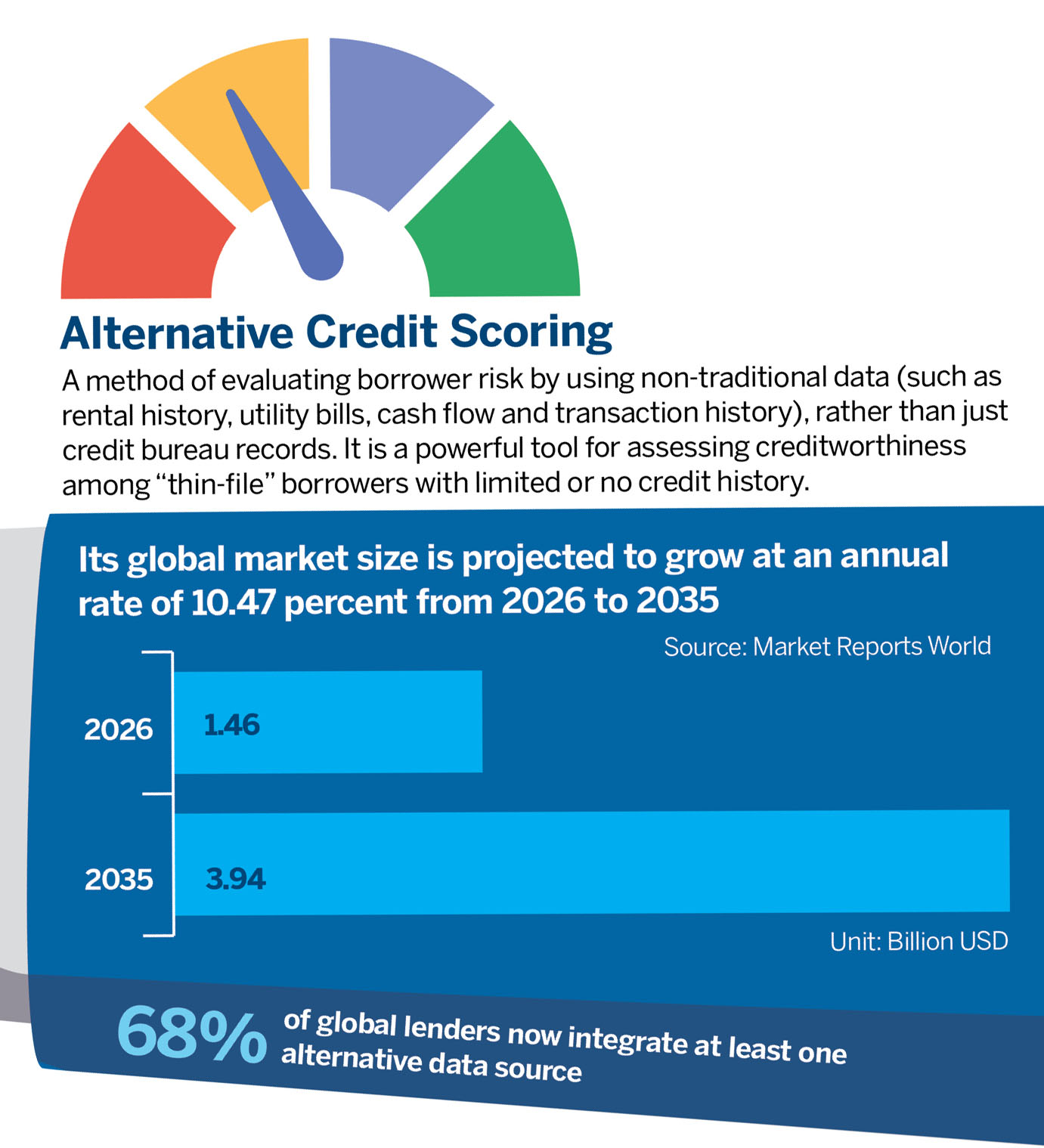

Thin credit files are not uncommon in Hong Kong, considering the city’s high number of newcomers. Data from the Census and Statistics Department show that about 25,000 new migrants arrived last year, and the number of foreign domestic workers has continued to recover after the COVID-19 pandemic.

For them, traditional credit-scoring models may struggle to accurately assess repayment capacity due to limited local credit histories, potentially leaving those who are creditworthy but unable to substantiate it without access to reasonable financing.

Globally, lenders are increasingly turning to alternative data to fill those gaps. Educational attainment, utility payments and mobile phone bills are being incorporated into underwriting models to refine risk assessment, Xiong says.

TransUnion, for example, is exploring the use of telecommunications data. Given that people today spend much of their time on mobile phones, Sin says behavioral data, such as borrowers’ mobile usage habits, could provide insights into the correlations with creditworthiness.

“In academia, we do have papers demonstrating that incorporating such alternative data into credit underwriting models could better predict the probability of default among borrowers,” Xiong says.

In Hong Kong, however, the deployment of alternative data in credit scoring remains relatively limited amid concerns over data privacy and security, says Sin.

“Over-indebtedness is a phenomenon, but the real problem is delinquency. And, when you see delinquency, it is already too late. What we are trying to do is to have a predictive score even when the borrower is still in the application stage or repaying normally, (and use it to identify whether) the borrower’s profile is skewed toward delinquency,” he says, adding that such tools will enable banks and licensed money lenders to act quickly.

In that sense, Hong Kong’s attempt to build a more transparent and sustainable money-lending sector may only be the beginning.

Next Actions

1. Strengthening enforcement and penalty frameworks, alongside sustained action against unlicensed lending.

2. Providing financial and technical support to smaller lenders to facilitate their integration with Credit Data Smart.

3. Reviewing the blanket 48-percent interest rate cap and allowing lower rates for borrowers with stronger credit profiles.

4. Encouraging responsible use of alternative data in credit assessments.

Source: Interviews and research

Contact the writer at irisli@chinadailyhk.com