Hong Kong’s once-quiet local currency bond market is quickly becoming one of Asia’s hottest funding venues, as corporate issuers seek stability in a city looking to lure more debt offerings.

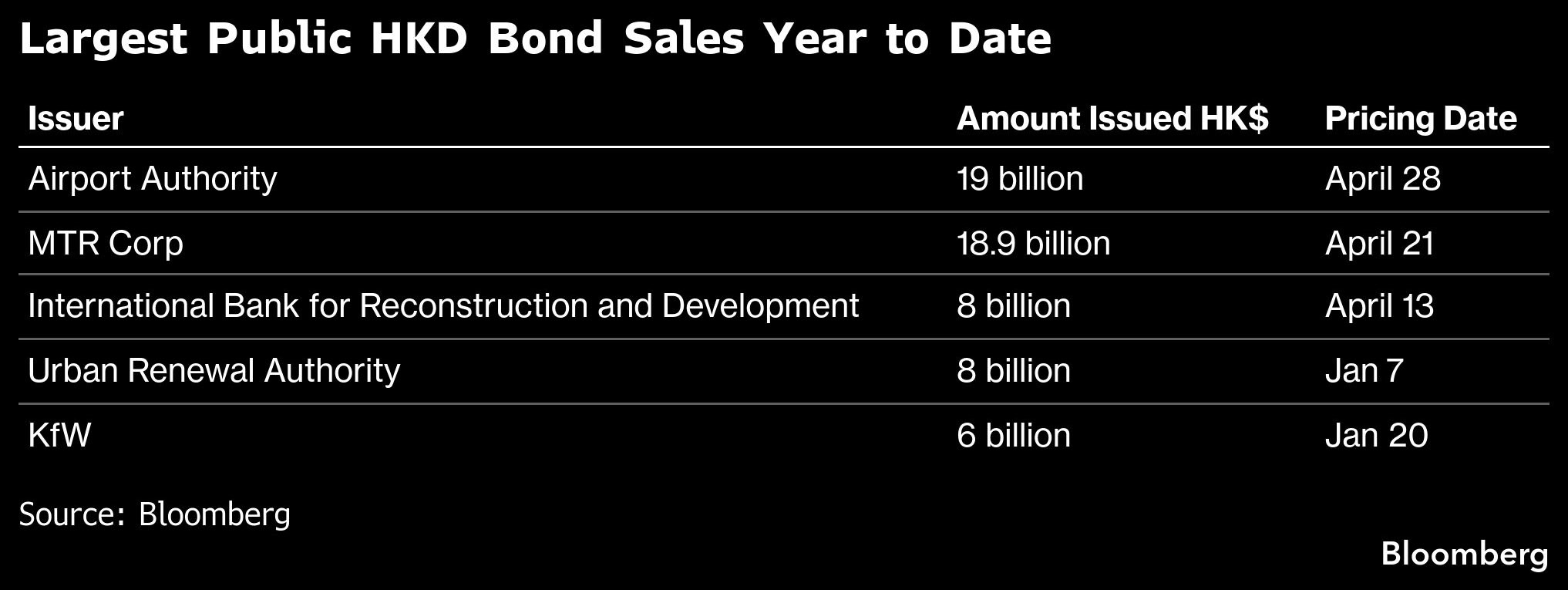

Global and local entities have raised a record HK$74 billion ($9.4 billion) through public Hong Kong dollar bond issuance so far this year — a big turnaround for a market that for years has struggled with tepid demand and limited issuers, who mainly focused on small-scale private deals.

Just this week, the local airport operator priced a HK$19 billion offering, the latest in a wave of deals coming as the city’s regulators push to position Hong Kong as a global fixed income hub.

ALSO READ: Hong Kong airport raises $2.4b amid local-debt boom

Hong Kong’s appeal as a safe haven amid turmoil in the Middle East and other regions has helped fuel the recent activity, putting the city’s around $360 billion local currency market on the radar of more issuers.

“We’ve been pitching hard for years to corporates because the Hong Kong dollar market deserves more attention, especially under current geopolitical uncertainties. It’s deep enough, it’s stable, and it offers real savings,” said David Yim, head of capital markets for Greater China and North Asia at Standard Chartered, a top arranger of such deals.

A confluence of factors has driven the shift. An increase in liquidity in the local banking system has led to cheaper funding costs, allowing issuers to price Hong Kong dollar bonds at tighter yields. Geopolitical risks are also fueling the trend — first the Trump administration’s widespread imposition of tariffs, and then the Iran war — making the local debt market more appealing to companies rethinking US dollar deals.

“Issuers are increasingly turning to local currencies when US dollar markets are volatile or expensive,” said Eugene Ng, head of debt capital markets for Greater China at HSBC, which is also a major arranger for local currency offerings.

For borrowers, pricing in the local currency has become more advantageous since the middle of last year, when the Hong Kong interbank offered rate dropped, widening the spread with US interest rates. That came after the Hong Kong Monetary Authority took steps to cool a rally in the local currency, which boosted liquidity in the market and lowered borrowing costs.

Because the Hong Kong dollar is pegged to the greenback, there’s little foreign exchange risk. That’s allowed issuers to borrow cheaply in Hong Kong dollars, convert into US dollars, and invest in higher‑yielding US Treasuries, locking in potential arbitrage gains.

ALSO READ: Capital inflows into HK continue amid global market uncertainties

“Hong Kong dollar rates have the steepest curves in developed markets and offer attractive carry,” said Lei Zhu, head of Asian fixed income at Fidelity International. Growth in long‑dated, green and digital bonds, supportive regulation and market deepening suggest that Hong Kong dollar credit is evolving from a tactical hedge into a long‑term strategic allocation, she added.

The rush of Hong Kong dollar public bond issuance has taken shape over the past 12 to 18 months as liquidity has grown at the city’s financial institutions. The Hong Kong dollar loan-to-deposit ratio has been below 75 percent since early last year — a level not seen since 2010, according to HKMA data as of February, indicating a burgeoning cash cushion.

That’s come amid a shortage of high‑quality assets to invest in, making domestic institutions such as insurers and pension funds eager buyers of bonds with solid credit profiles and stable yields.

Among the issuers, MTR Corp Ltd, the government‑backed public transport operator and property developer, just priced its first‑ever public Hong Kong dollar bond, raising HK$18.888 billion — a size that would have been impossible in private deals. Flagship airline Cathay Pacific and the World Bank’s lending arm have also sold notes in recent weeks.

READ MORE: MTR seeks $1.9b in public Hong Kong dollar bond sale

HSBC, Standard Chartered Bank, Bank of China (Hong Kong) and Credit Agricole CIB are some of the top banks arranging Hong Kong dollar bond deals, according to Bloomberg-compiled data.

Hong Kong dollar bond sales have offered the cheapest cost of funds this year for issuers such as MTR, said Terry Schmassmann, co-head of debt capital markets Asia and head of DCM syndicate Asia at UBS. The company will be able to get close to 10 basis points of arbitrage gains on the five‑year and 10‑year notes just sold, he added.

“Is this a lasting trend? It’s still too early to tell,” Schmassmann said. “So far, it’s been a very high‑grade, domestic‑name market, but diversification is clearly driving interest.”