Insurance-linked securities can be a catalyst in driving sustainable and diversified development of Hong Kong’s financial services. But, the nascent market ecosystem needs substantial improvements in data infrastructure, market liquidity and investor awareness. Oswald Chan reports.

Editor’s note: Hong Kong is strengthening its global financial center status for companies to better manage business and financial risks. The first part of this series examines how catastrophe bonds can beef up financial services’ risk management functions, and make the city the world’s largest cross-border wealth management hub.

Talking about Hong Kong as a global financial hub conjures up images of how much funding the city’s equity market raises or the size of the wealth it manages.

The magnitude of Hong Kong’s stock market and assets under management affirms that the city is one of the world’s premier finance centers. But, it can’t afford to rest on its laurels — it must go beyond equity fundraising and asset and wealth management.

The Hong Kong Special Administrative Region government has to continue devising ways of expanding the system’s functions to make the financial sector more diversified, resilient and sustainable.

READ MORE: Hong Kong’s strengths to aid global green transition, say Chan

Insurance-linked securities (ILS), including catastrophe bonds (CAT bonds), have been identified as a key segment for driving the growth of the SAR’s financial services business.

ILS are financial instruments that transfer specific risks such as those caused by natural disasters like hurricanes or earthquakes to capital market investors.

As a subset of ILS, CAT bonds have become an increasingly popular alternative asset class. In the absence of a disaster triggering losses for investors, CAT bonds can offer highly attractive yields and risk-adjusted returns with low volatility and low correlation to traditional assets, while CAT bond issuance sponsors can alleviate and diversify risks, gain access to capital sources and raise funds.

The emergence of such an asset class as a growing mainstream financial instrument comes as the climate crisis spawns a surge in the frequency and intensity of extreme weather events.

Earlier this year, a sprawling winter storm left hundreds of thousands of people without power in the United States, while severe flooding wreaked havoc across large parts of Mozambique, South Africa and Zimbabwe, and a major heat wave gripped southeastern Australia.

This explains why the global CAT bond market, in terms of issuance, the number of sponsors and market size, is growing.

According to specialist data provider Artemis.bm, CAT bond issuance rose to $25.6 billion last year, surpassing the 2024 record of nearly $17.7 billion by a whopping 45 percent. The issuance stemmed from 122 transactions — exceeding the previous high of 95 in 2023 — with 15 first-time sponsors entering the market. The outstanding catastrophe bond market hit a record $61.3 billion last year — up 24 percent from nearly $49.5 billion in 2024.

Ecosystem challenges

China’s 14th Five-Year Plan (2021-25) first articulated the vision of supporting Hong Kong as an international business and financial risk management pivot by promoting the insurance industry’s competitiveness. Following the State Council’s outline in February 2019 to back the city as a risk management center, the China Banking and Insurance Regulatory Commission pledged to help Chinese mainland insurers issue CAT bonds in Hong Kong.

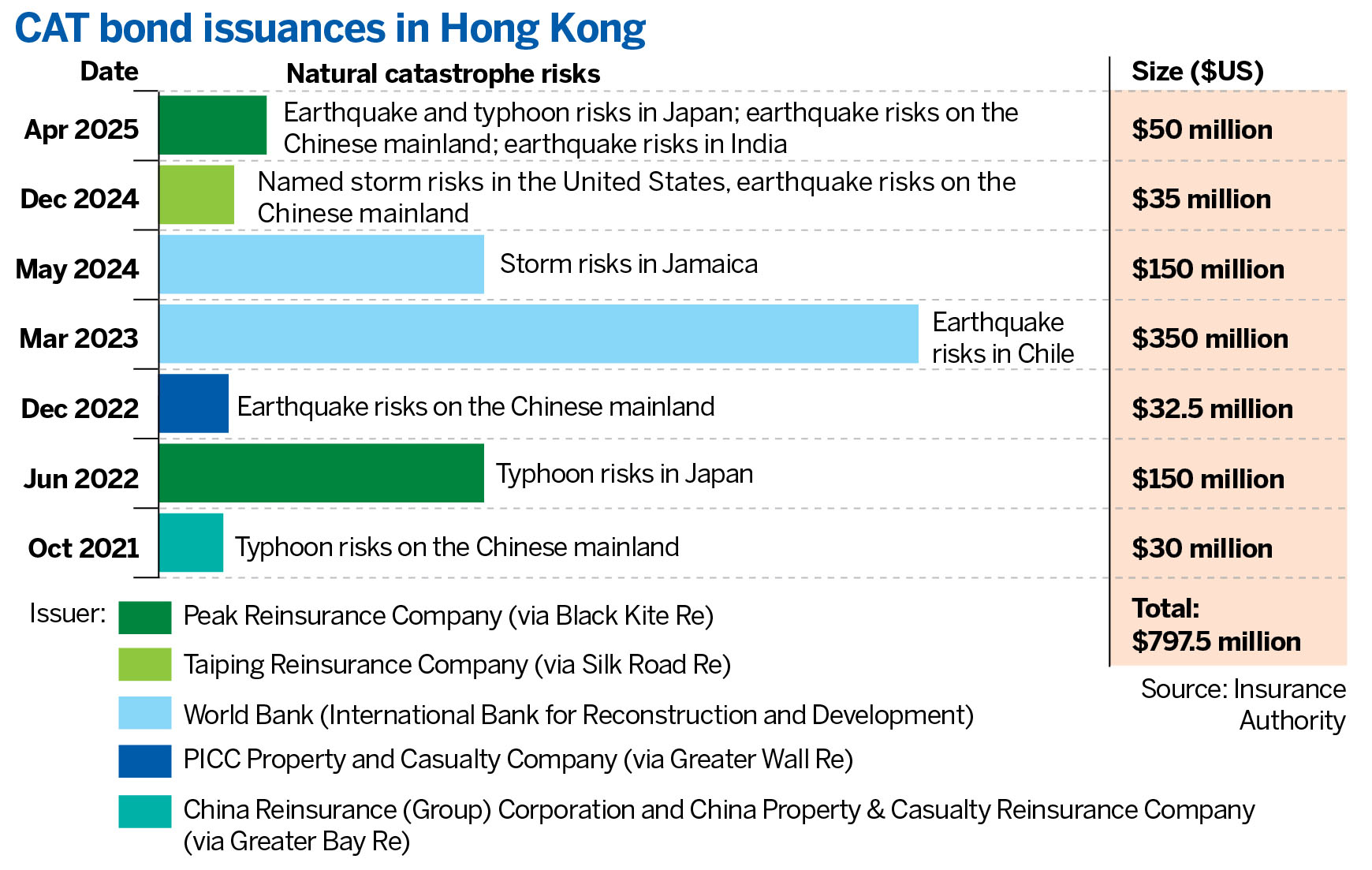

The Insurance Authority (IA) said almost $800 million worth of ILS in the form of CAT bonds have been issued in Hong Kong since October 2021. The issuers ranged from mainland reinsurance companies to international organizations like the World Bank, with insurance products hedged mainly against typhoon and earthquake risks on the mainland and in Japan, India, Chile, Jamaica and the US.

Despite the growth, Hong Kong’s CAT bond issuance ecosystem is still nascent as the ecosystem lacks data infrastructure and modeling capacity, market depth, as well as investor awareness. In natural catastrophe coverage, Hong Kong is devoid of reliable environmental data, hindering risk assessment and underwriting in the bond issuance process.

“Hong Kong should attract global climate scientists, reinsurers and modeling firms to build a regional catastrophe data hub, especially to serve the Guangdong-Hong Kong-Macao Greater Bay Area and the Asia-Pacific. There is room for improvement in cross-disciplinary integration among climate scientists, actuaries and capital market professionals,” says Lionel Mok Wing-fung, sustainable finance program lead at Civic Exchange — a Hong Kong-based thinktank that focuses on sustainability.

“To ensure data quality, Hong Kong should invest in standardized environment data collection systems, such as satellite monitoring, artificial intelligence-based weather analytics, and region-specific seismic databases,” he says.

Mok says it is important for Hong Kong to build up its proprietary modeling capability to strengthen price credibility and reduce reliance on foreign analytics firms. “If we can provide data tailored to Asian typhoon, flooding and earthquake risks, and incorporate forward-looking climate scenarios, rather than just historical data, it would differentiate Hong Kong from other CAT bond issuance centers like Bermuda and Singapore.”

Cyrus Cheung Lap-kwan, Greater China divisional president and environmental, social and governance committee chair 2026 of CPA Australia, suggests Hong Kong’s financial industry can access the data from the Hong Kong Observatory and even the World Meteorological Organization to structure CAT bonds.

Hong Kong has to step up investments in AI and satellite applications to access real-time data in CAT bond structuring, and the “negative impact of a data gap on the pricing and term structuring of CAT bonds will be increasingly narrowed, with better technological advancement and availability of financial services expertise”, says Cheung.

The IA is spearheading collaboration among the regulator, industry and academia in conducting a climate modeling project to boost climate risk management capabilities, improve underwriting practices, and develop products that are both commercially viable and effective in bridging the wealth protection gap.

The second challenge is the absence of market depth in Hong Kong’s CAT bond market. Liquidity remains a structural challenge as CAT bonds issued locally are typically traded in the secondary over-the-counter market.

“Hong Kong could explore listing CAT bonds on exchange platforms or developing a dedicated ILS trading segment to enhance price transparency. The government can also expand granting incentives to include market-making and encourage global ILS funds to trade in Hong Kong-issued CAT bonds. Collaboration with mainland institutional investors could further deepen liquidity pools,” Mok tells China Daily.

Boosting market depth

Given that the number of CAT bond issuances in Hong Kong is still small, Cheung says it is vital to attract more global sponsors. “When there are more issuances, it would eventually boost transactions and hence the liquidity of the secondary market.”

“Aggregating more global asset managers, such as insurers and pension funds, to Hong Kong is also crucial in boosting the CAT bond market ecosystem as they are among the sources of capital and managers of financial assets”, says Rocky Tung Yat-ngok, executive director of the Financial Services Development Council (FSDC) — a high-level and cross-sectoral advisory body of the SAR government tasked with promoting the development of financial services.

The third element of cementing the ecosystem is elevating investors’ awareness of CAT bonds as an alternative financial asset. “The FSDC is considering cross-teaching sessions for insurance companies’ product specialists and private banks’ relationship managers to strengthen their product knowledge and enhance mutual interactions between them,” says Tung.

“Hong Kong may be proficient in providing single investments like stocks, but it is not the top financial jurisdiction in alternative investments. By developing the CAT bond market, we can make Hong Kong’s capital market more comprehensive and diversified, and this will help make the SAR a safe haven for global capital,” he says.

The IA will host the third edition of the annual ILS Conference in Hong Kong this month, which is expected to attract over 100 insurers, asset managers, institutional investors and professional service providers from across Asia to explore ways of developing investor interest and capacity.

Hong Kong is aggressively expanding its role as a premier ILS hub by extending financial subsidies, bolstering market regulatory framework and providing tax concessions.

The SAR government recently extended the Pilot Insurance-linked Securities Grant Scheme, which was initiated in 2021, to 2028, offering subsidies to eligible ILS issuances in Hong Kong to offset a maximum of 100 percent of total upfront costs, up to HK$7 million for new issuance.

Following the passage of the Insurance (Amendment) Bill 2020 in July that year, the IA introduced a special purpose insurer regime to offer simplified reporting requirements and shorter processing time for authorizing ILS issuances. The Insurance (Special Purpose Business) Rules have also been amended to slash the minimum investment threshold for sophisticated investors investing in CAT bonds from the initial $1 million to $250,000.

Hong Kong may also expand the preferential tax regimes for funds, carried interest, and single-family offices’ family-owned investment holding vehicles, with ILS as one of the qualifying asset classes for investors to enjoy such preferential tax treatment. The administration hopes the amendment bill will be passed by the end of June, targeting an effective implementation date from the 2025-26 tax assessment year.

“We’ll study the feasibility of introducing a legislative framework for protected cell companies and review the current definition of eligible ILS investors under the Insurance (Special Purpose Business) Rules to explore expanding its scope, with a view to enabling greater flexibility and cost-efficiency for ILS issuers, while balancing with investor protection,” says IA Policy and Legislation Executive Director Clement Lau Chung-kin.

Proactively encouraging issuance of CAT bonds is in line with Hong Kong’s goal of becoming a world risk management hub and realizing its vision of promoting the asset and wealth management sector, with the demand-supply dynamics of the CAT bond market being increasingly favorable, experts say.

On the supply side, infrastructure development in the Greater Bay Area increases exposure to climate and other disaster risks that incentivize project owners and reinsurance companies to consider whether they can mitigate certain risks through securitization, says Cheung.

According to Tung, Hong Kong, with its open capital account and the capability to access international investors, is the right jurisdiction for CAT bond issuers.

“We are seeing corporate entity participation in ILS issuances, and the companies have extended the integration of risk transfer mechanisms against extreme weather events — by way of ILS — into construction or infrastructure projects,” notes Lau.

ALSO READ: HK, mainland financial market to forge deep, proactive alignment

The IA executive director says the insurance industry watchdog is engaging potential mainland sponsors, local and supranational organizations to issue CAT bonds in Hong Kong. “Hong Kong’s unique connectivity with the mainland enables us to leverage our close proximity to a deep natural-catastrophe risk pool.”

The demand side is working favorably, too. With the SAR betting it’ll become the world’s largest cross-border wealth management center in the coming years, cementing the CAT bond market’s development will help various asset managers, including sovereign wealth funds, pension funds and family offices, to tap into this alternative asset class.

“Hong Kong and mainland financial regulators can study whether alternative asset class like CAT bonds can be included in the cross-border wealth management connect program between Hong Kong and the mainland,” says Cheung.

Mok believes that combining the demand and supply dynamics will create a virtuous circle favorable to the market’s development.

“Infrastructure expansion drives supply, while cross-border wealth integration stimulates demand, creating a reinforcing ecosystem.”

Contact the writer at oswald@chinadailyhk.com